LIC Surrender Value Calculator: How Much Will You Get?

Are you planning to cancel your Life Insurance Corporation (LIC) policy before its maturity? Whether you are facing a financial emergency, are unsatisfied with the policy returns, or simply cannot afford the premiums anymore, surrendering your LIC policy is a major financial decision.

Before you submit that cancellation form, it is crucial to know exactly how much money you will get back. This is where an LIC Surrender Value Calculator comes in.

In this comprehensive guide, we will break down what surrender value is, the key factors that influence your return, how it is calculated with practical examples, and whether surrendering is the right choice for your financial future.

What is LIC Surrender Value?

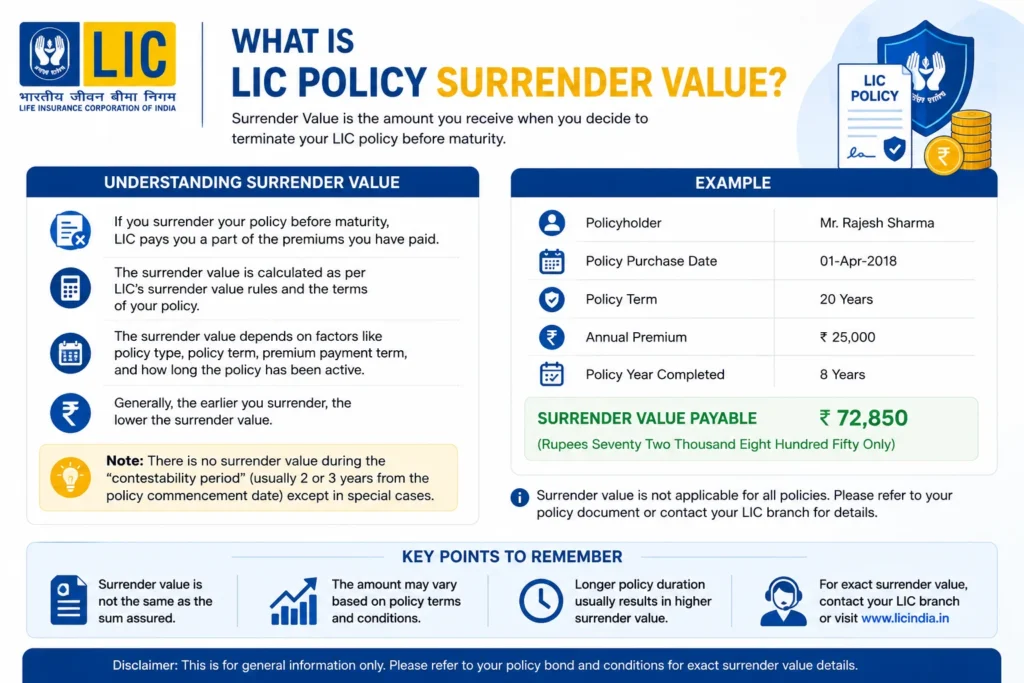

When you terminate your life insurance policy before its actual maturity date and withdraw the cash value it has accumulated over the years, the amount paid back to you by LIC is called the Surrender Value. It acts as a partial refund of the premiums you have paid.

When you surrender a policy, two things happen immediately:

- Your life cover (death benefit) ceases to exist.

- The policy contract is permanently terminated.

Important Rule: To be eligible for a surrender value, you must have paid your premiums continuously for a minimum lock-in period. Traditionally, this is 3 full years, though some newer plans under recent IRDAI guidelines may acquire a surrender value after just 2 years. If you cancel before this lock-in period, your policy lapses and you receive nothing.

Key Factors Affecting Your LIC Surrender Value

The surrender value is not a random figure; it is mathematically derived based on several dynamic elements of your policy. Here are the primary factors that determine how much you will receive:

- Number of Premiums Paid: The longer you stay invested, the higher your surrender value. Surrendering in the 3rd year will yield a much lower percentage of your paid premiums compared to surrendering in the 15th year.

- Total Premium Amount: Higher annual premiums naturally translate to a larger accumulated cash value over time.

- Policy Term (Tenure): The surrender value factor applied by LIC is heavily influenced by the total duration of the policy. A policy nearing its maturity will have a significantly higher surrender value factor than one that has just completed its lock-in period.

- Accrued Bonuses: Participating policies (like Endowment and Money Back plans) accumulate Simple Reversionary Bonuses and sometimes Final Additional Bonuses. A portion of these accrued bonuses is added to your final payout.

- Type of Policy: Traditional endowment plans and ULIPs (Unit Linked Insurance Plans) have entirely different surrender structures. Term insurance plans, on the other hand, do not have any surrender value at all.

How is the LIC Surrender Value Calculated?

LIC calculates your final payout based on two different methods. The final amount credited to your bank account is always the higher of the two:

1. Guaranteed Surrender Value (GSV)

GSV is the legally guaranteed minimum amount you will receive upon cancellation. It is calculated as a fixed percentage of the total premiums you have paid, excluding the first year's premium and any extra premiums paid for riders (like accidental death benefit).

- General Formula: (Total Premiums Paid - First Year Premium) x GSV Factor + (Accrued Bonuses x Bonus Surrender Factor)

2. Special Surrender Value (SSV)

The SSV is usually higher than the GSV and depends on the duration the policy has been active, the total sum assured, and the paid-up value.

- General Formula: (Paid-Up Value + Accrued Bonuses) x SSV Factor

- Paid-Up Value Formula: (Number of Premiums Paid / Total Number of Premiums Payable) x Basic Sum Assured

How Surrender Value Grows Over Time

To understand how the surrender penalty decreases and your cash value increases over time, let us look at a hypothetical example.

Scenario: * Policy: LIC New Endowment Plan

- Sum Assured: ₹5,00,000

- Policy Term: 20 Years

- Annual Premium: ₹25,000

The table below illustrates the approximate Surrender Value at different stages of the policy:

| Year of Surrender | Total Premiums Paid | Approx. GSV Factor | Accrued Bonus Value (Estimated) | Estimated Surrender Value | Recovery Percentage |

|---|---|---|---|---|---|

| Year 2 | ₹50,000 | 0% | ₹0 | ₹0 | 0% (Loss) |

| Year 3 | ₹75,000 | 30% | ₹10,000 | ₹25,000 | 33% (Heavy Loss) |

| Year 5 | ₹1,25,000 | 50% | ₹30,000 | ₹80,000 | 64% (Moderate Loss) |

| Year 10 | ₹2,50,000 | 65% | ₹90,000 | ₹2,37,000 | 94% (Slight Loss) |

| Year 15 | ₹3,75,000 | 75% | ₹1,75,000 | ₹4,37,500 | 116% (Profitable) |

Note: The above figures are estimates for educational purposes. Exact values depend on LIC's officially declared bonus rates and prevailing SSV factors).

Expected Surrender Value by LIC Plan (Approximations)

Different LIC plans yield different returns upon surrender. Endowment plans typically offer better surrender values than money-back plans (since money-back plans pay out survival benefits periodically).

| LIC Plan Name | Surrender Value Percentage (Approx.) |

|---|---|

| LIC Jeevan Anand | 30% to 80% of total premiums paid depending on policy age |

| LIC New Endowment Plan | 30% to 70% of total premiums paid depending on policy age |

| LIC Money Back Plans | 30% to 50%, depending on survival benefit payouts already received |

| LIC Jeevan Labh | 30% to 75%, depending on premium paying term and duration |

| LIC Jeevan Umang | 40% to 80%, depending on duration and premium paying term |

Alternatives to Surrendering Your LIC Policy

Surrendering your policy early almost always results in a financial loss, as the surrender value factors in the early years are quite low. Before taking the hit, consider these highly recommended alternatives:

1. Make the Policy "Paid-Up"

If you can no longer afford the premiums but do not need the cash immediately, you can stop paying and convert the policy to a "Paid-Up" status. Your life cover continues, but at a proportionately reduced Sum Assured. You will receive this money at the original maturity date along with bonuses accrued up to the date you stopped paying, saving you from heavy surrender penalty deductions.

2. Take a Loan Against Your LIC Policy

If you need urgent cash for a financial emergency, LIC offers loans against policies that have acquired a surrender value. The interest rates are highly competitive (often much lower than personal bank loans), and your life insurance coverage remains fully active for your family's financial security.

How to Use the LIC Policy Surrender Value Calculator

Using an online calculator simplifies the complex mathematics behind GSV and SSV. To get an accurate estimate, you will need to input:

- Your specific LIC Policy Plan Name

- Basic Sum Assured

- Policy Term (in years)

- Annual Premium Amount

- Number of Years Premiums have been paid

- Accrued Bonuses (can be checked via the LIC customer portal)

Once entered, the tool automatically applies the correct GSV and SSV factors to give you an instant estimate of your return, along with a percentage showing your exact profit or loss.

FAQs on LIC Surrender Value Calculator

What is surrender value in an LIC policy?

The surrender value is the amount paid by LIC to the policyholder if they cancel the policy before maturity. It is essentially a partial refund of the premiums paid minus early termination charges

When can I get a surrender value for my LIC policy?

You can get the surrender value only after paying premiums continuously for at least 3 full years. (For some specific newer plans, this is 2 years). If surrendered before this lock-in period, no surrender value is payable.

How is LIC surrender value calculated?

It is calculated using a standard formula based on total premiums paid (excluding the first year), surrender value factors defined by LIC, and accrued reversionary bonuses, if any.

What is Guaranteed Surrender Value (GSV)?

GSV is the minimum amount guaranteed by LIC on policy surrender. It is a percentage of premiums paid excluding the first-year premium. After 3 years, the surrender value gradually increases with each additional year’s premium paid.

What happens to bonuses on surrender?

Applicable vested bonuses up to the surrender date are added to the surrender value for participating policies. However, they are multiplied by a Bonus Surrender Factor, meaning you receive a discounted portion of the bonus, not the full amount.

Is LIC surrender value taxable?

If you surrender your policy before completing 5 years, the surrender value becomes taxable according to your income tax slab, and previous Section 80C deductions may be reversed. If surrendered after 5 years, it is generally tax-free under Section 10(10D), provided your annual premium did not exceed 10% of the sum assured.

Conclusion

The LIC Surrender Value Calculator is an essential online tool for LIC policyholders who need to understand how much they will receive if they decide to surrender their policy before maturity. It helps estimate the payable amount instantly based on various parameters such as premiums paid, policy term, accrued bonuses, and surrender value factors, taking the guesswork out of complex calculations.

Try Others Calculators